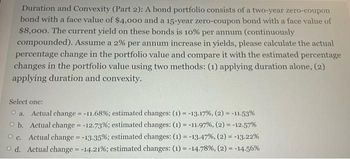

44 duration zero coupon bond

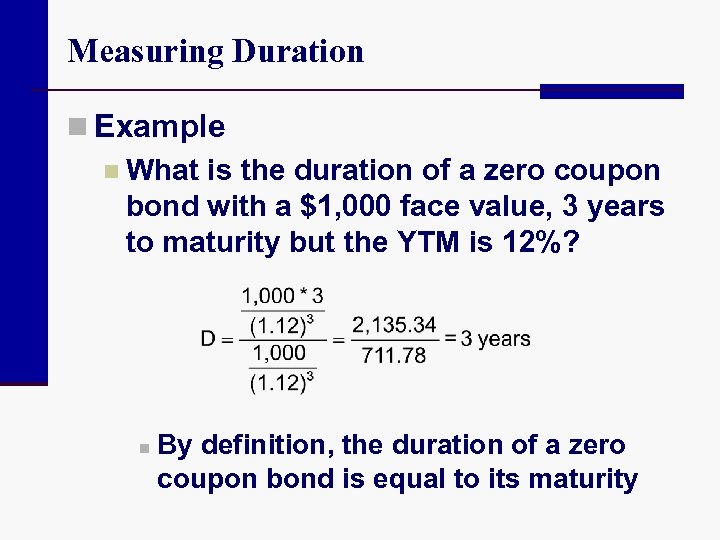

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far. How to Calculate Yield to Maturity of a Zero-Coupon Bond Sep 23, 2022 · Zero-Coupon Bond YTM Example . Consider a $1,000 zero-coupon bond that has two years until maturity. The bond is currently valued at $925, the price at which it could be purchased today. The ...

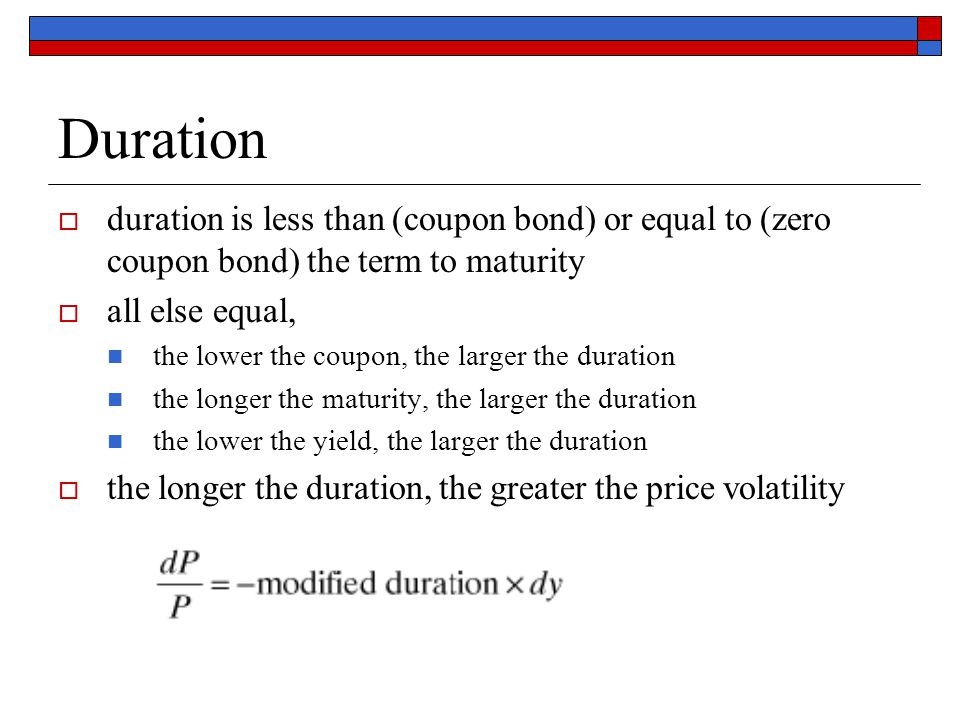

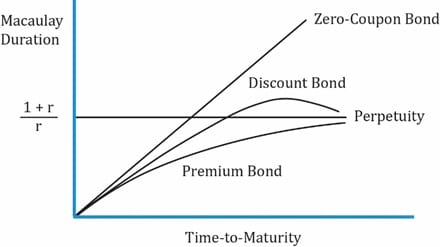

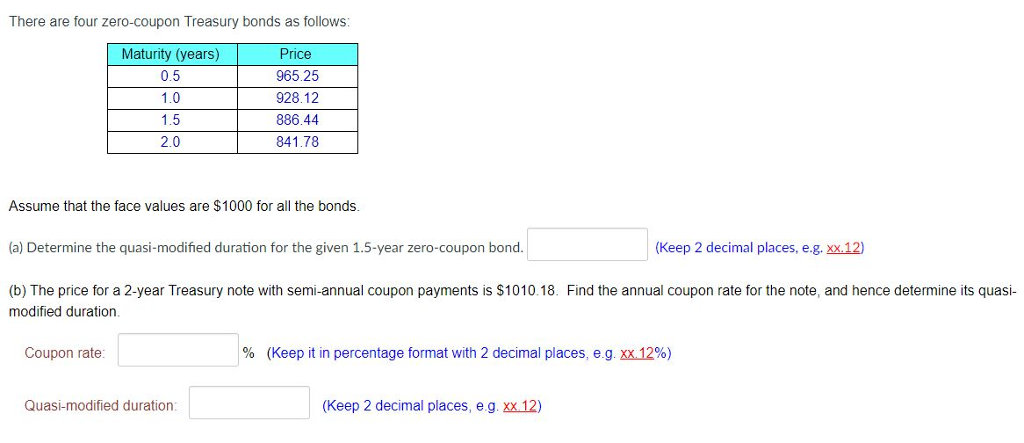

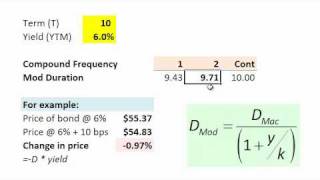

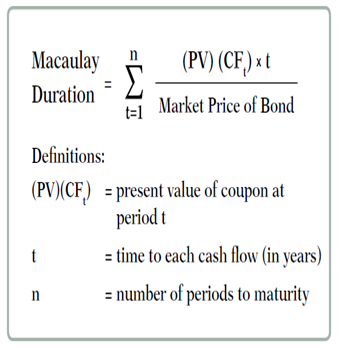

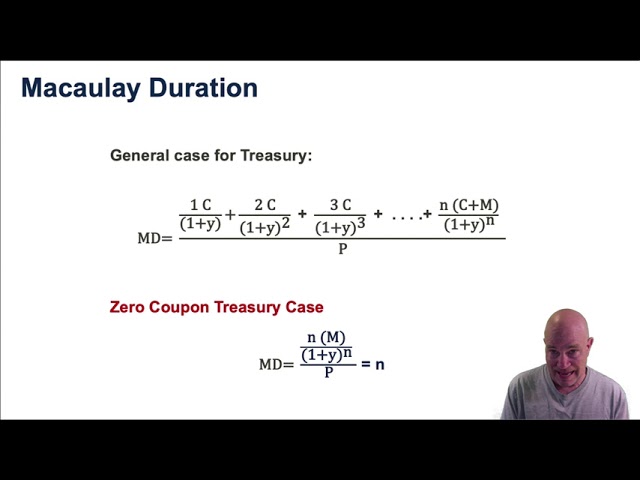

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

Duration zero coupon bond

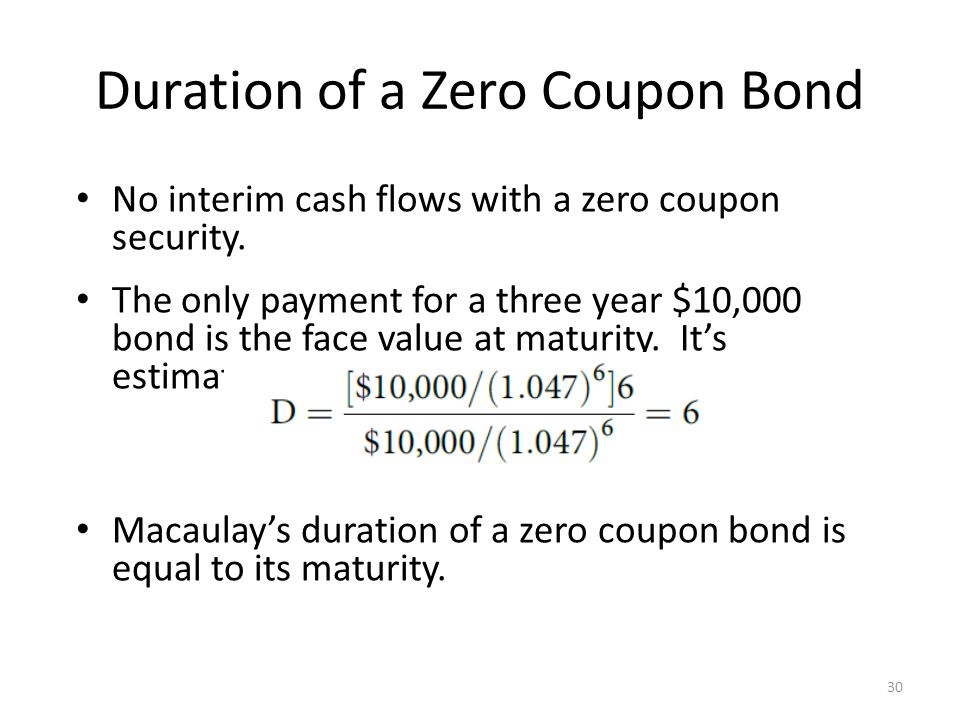

Coupon (finance) - Wikipedia In finance, a coupon is the interest payment received by a bondholder from the date of issuance until the date of maturity of a bond. Coupons are normally described in terms of the "coupon rate", which is calculated by adding the sum of coupons paid per year and dividing it by the bond's face value. For example, if a bond has a face value of ... What Is Duration of a Bond? - TheStreet Definition - TheStreet Oct 03, 2022 · The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity. When a coupon is ... Duration Definition and Its Use in Fixed Income Investing Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ...

Duration zero coupon bond. Zero Coupon Bond Value Calculator: Calculate Price, Yield to ... Instead interest is accrued throughout the bond's term & the bond is sold at a discount to par face value. After a user enters the annual rate of interest, the duration of the bond & the face value of the bond, this calculator figures out the current price associated with a specified face value of a zero-coupon bond. Duration Definition and Its Use in Fixed Income Investing Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ... What Is Duration of a Bond? - TheStreet Definition - TheStreet Oct 03, 2022 · The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity. When a coupon is ... Coupon (finance) - Wikipedia In finance, a coupon is the interest payment received by a bondholder from the date of issuance until the date of maturity of a bond. Coupons are normally described in terms of the "coupon rate", which is calculated by adding the sum of coupons paid per year and dividing it by the bond's face value. For example, if a bond has a face value of ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

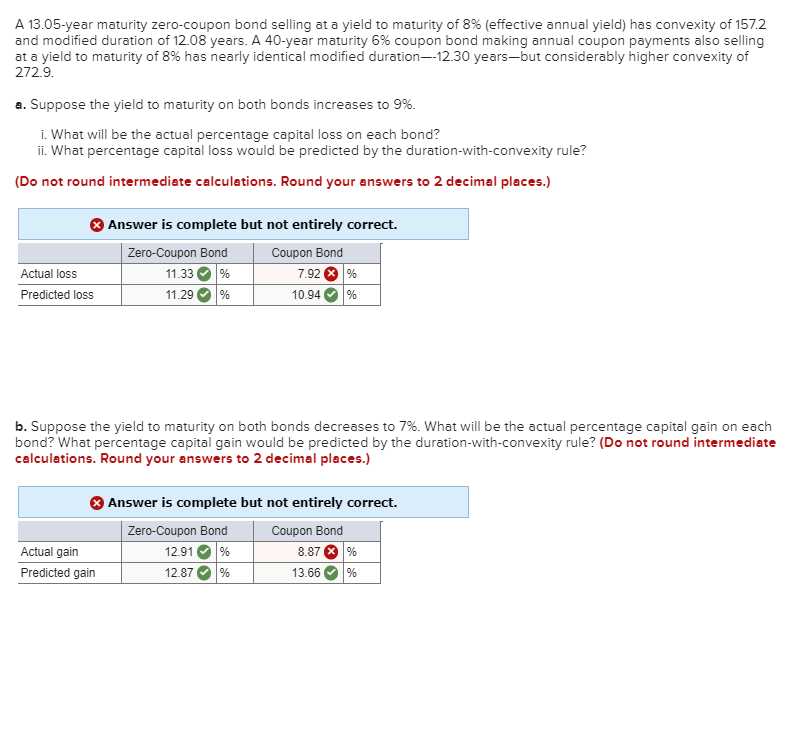

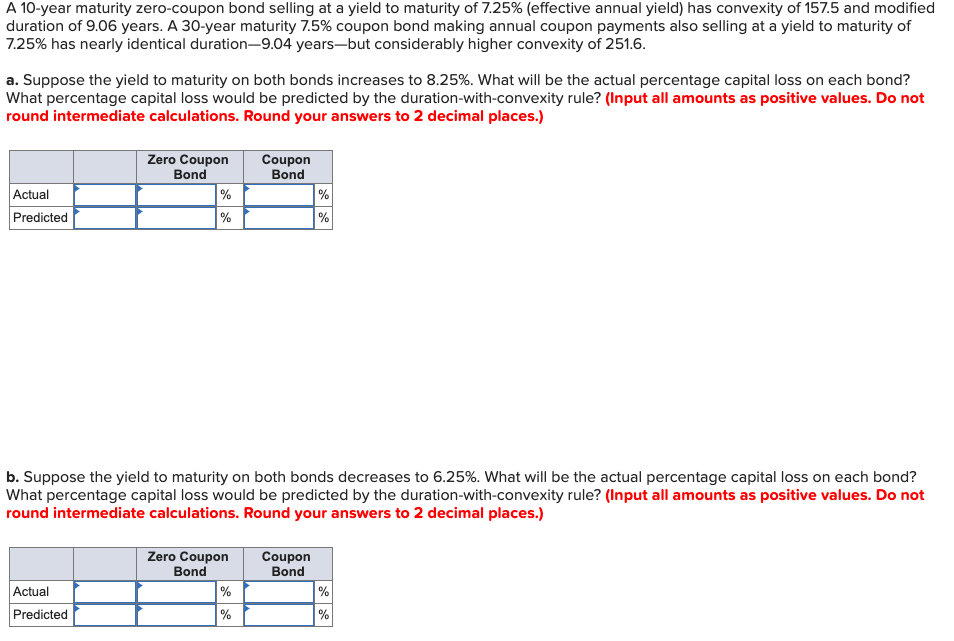

Solved A 13.05-year maturity zero-coupon bond selling at a ...

Solved A 13.35-year maturity zero-coupon bond selling at a ...

Bond Duration Flashcards | Quizlet

FRM: Dollar duration of zero coupon bond

Duration and Convexity, with Illustrations and Formulas

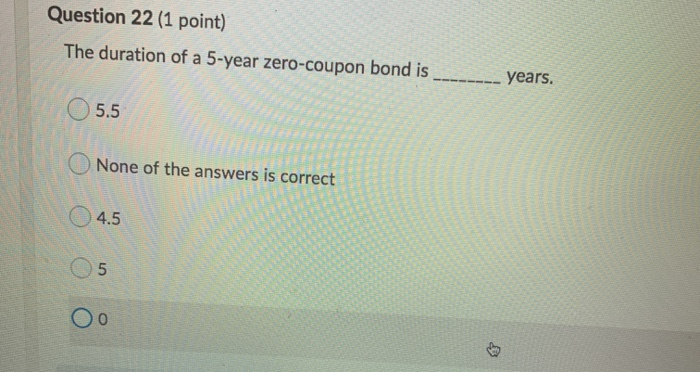

Solved Question 22 (1 point) The duration of a 5-year | Chegg.com

How to Calculate PV of a Different Bond Type With Excel

Zero-coupon bond price as a function of time to maturity for ...

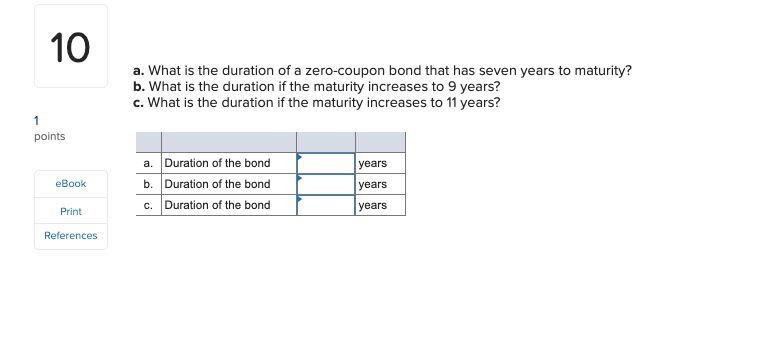

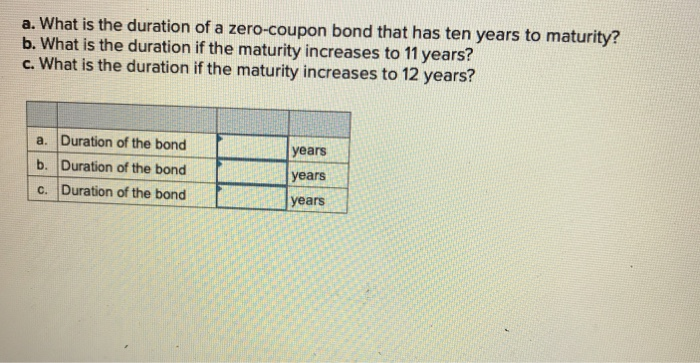

Solved a. What is the duration of a zero-coupon bond that ...

Zero-Coupon Bond: What are Zero-Coupon Bonds?

Bond Price Volatility Zvi Wiener Based on Chapter 4 in ...

Duration and Zero Coupon Bonds - YouTube

Bond Formula | How to Calculate a Bond | Examples with Excel ...

Solved A 10-year maturity zero-coupon bond selling at a ...

Portfolio Duration and its Limitations | CFA Level 1 ...

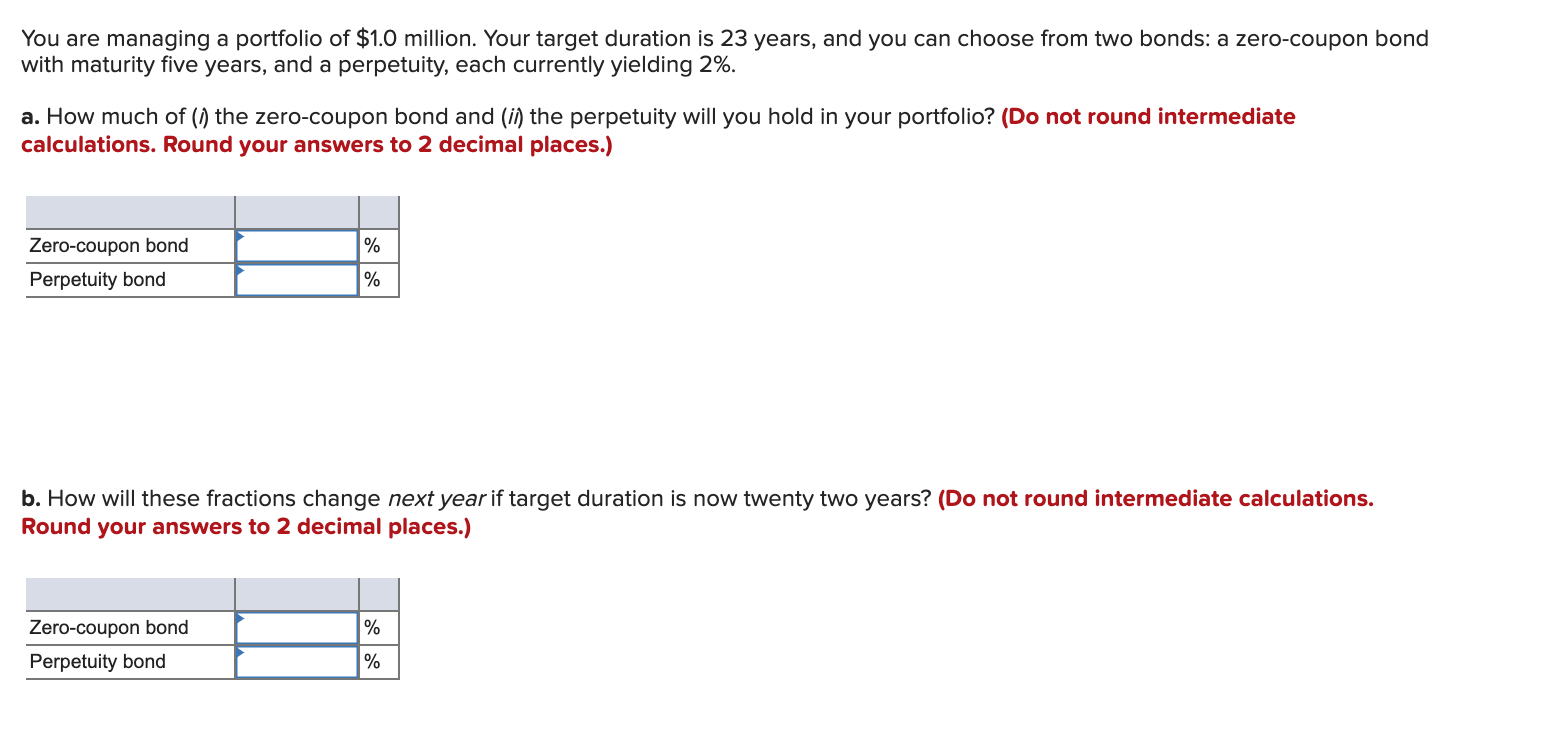

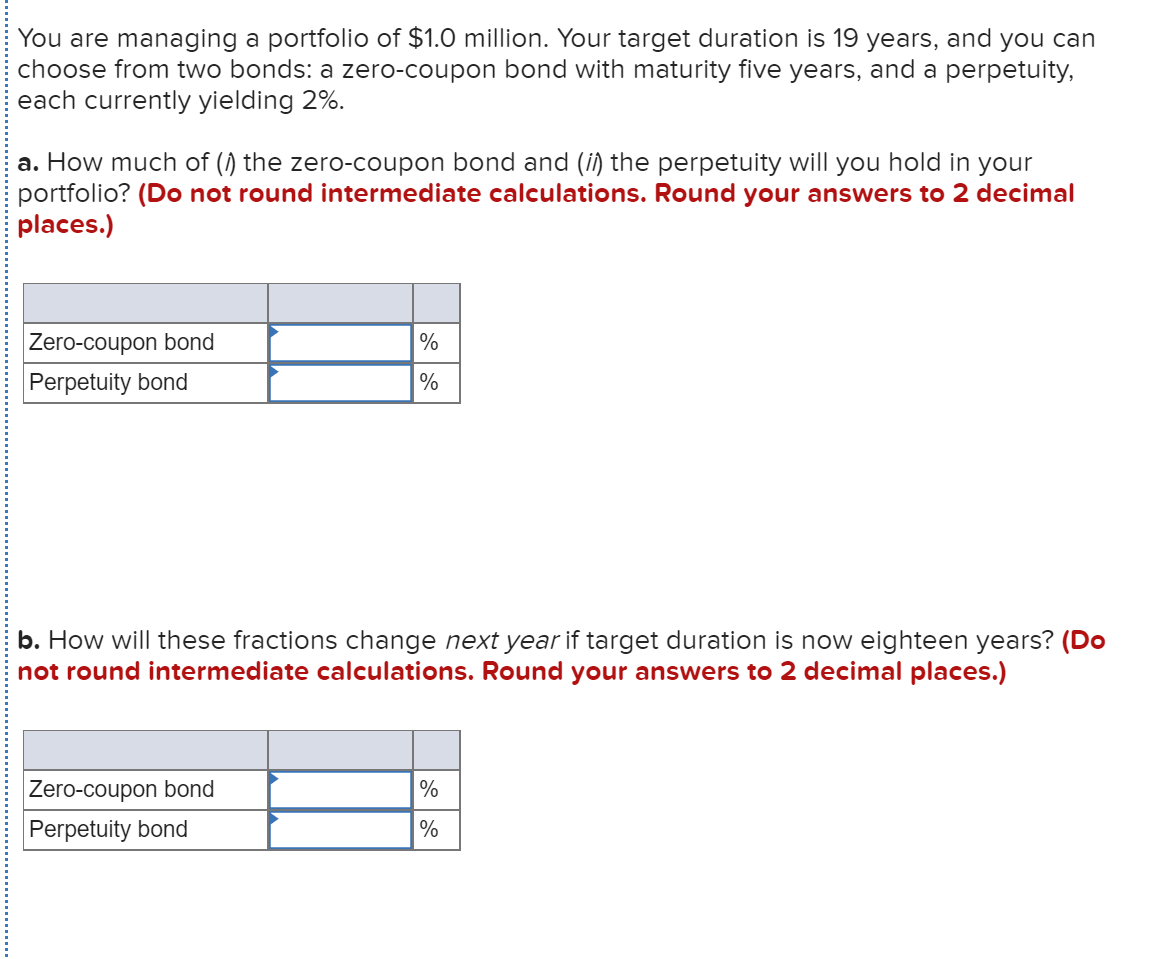

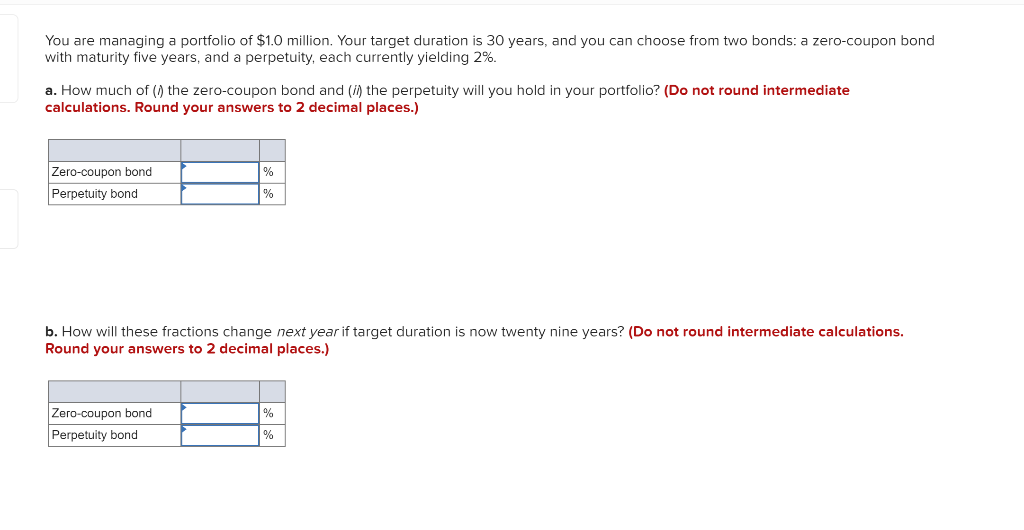

Solved You are managing a portfolio of $1.0 million. Your ...

Bonds of Mass Destruction - The Last Bear Standing

Solved You are managing a portfolio of $1.0 million. Your ...

Solved a. What is the duration of a zero-coupon bond that ...

Chapter 4 Bond Price Volatility. - ppt video online download

Understanding Fixed-Income Risk and Return | IFT World

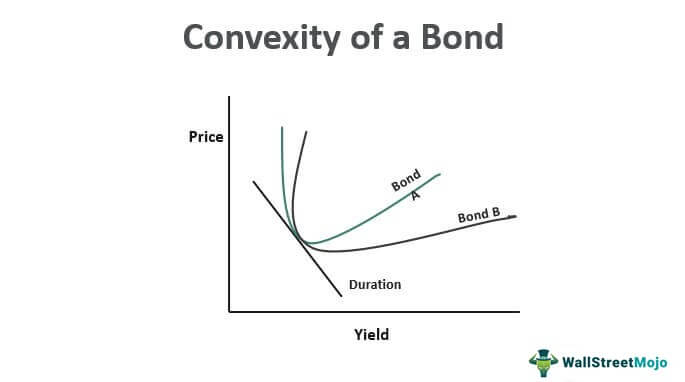

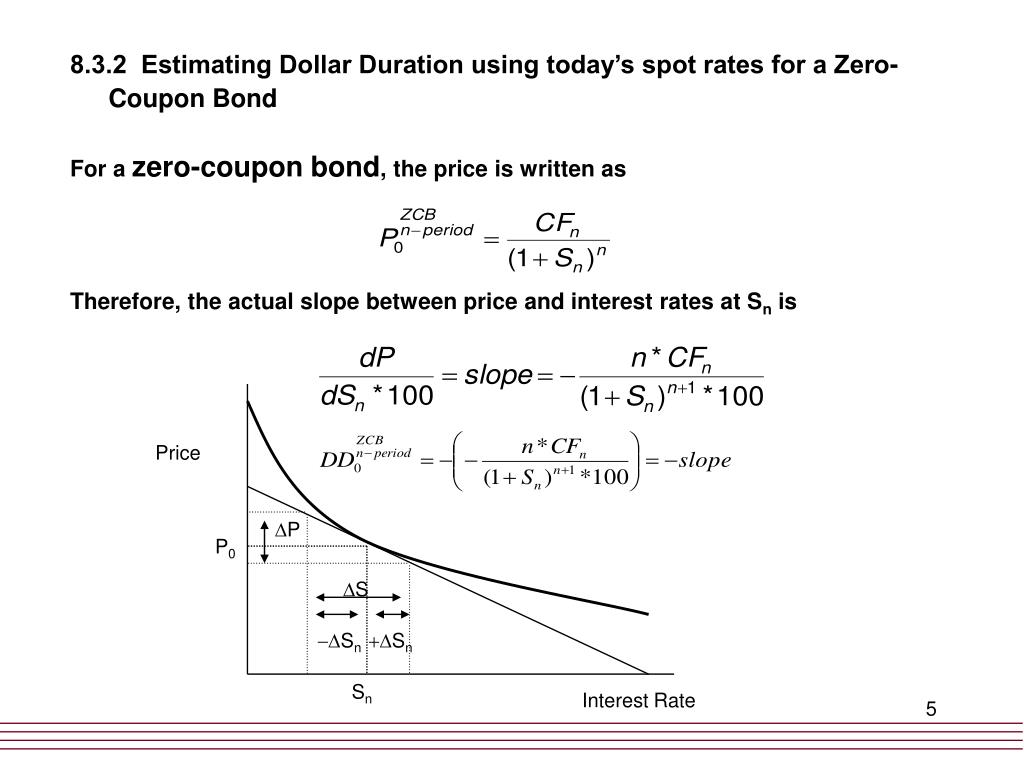

Convexity of a Bond | Formula | Duration | Calculation

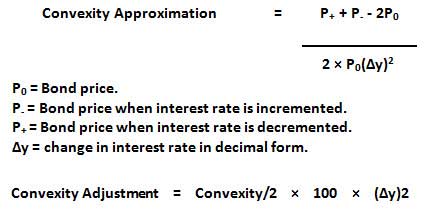

Solved There are four zero-coupon Treasury bonds as follows ...

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents

Modified duration of zero-coupond bond (FRM practice question ...

Solved] You are managing a portfolio of $3.0 million. Your ...

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

Convexity of a Bond | Formula | Duration | Calculation

Duration Analysis

WWWFinance - Bond Valuation: Campbell R. Harvey

The Key To Duration: Sensitivity To Changing Interest Rates ...

Duration and Zero Coupon Bonds - YouTube

Taylor Expansion To measure the price response to a small ...

Chapter 6: Pricing Fixed-Income Securities 1. Future Value ...

Answered: Duration and Convexity (Part 2): A bond… | bartleby

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

Price of a defaultable zero coupon bond price in each time t ...

Bank Management 6 th edition Management Timothy W

Zero Coupon Bond Value - Formula (with Calculator)

How Do I Calculate Yield To Maturity Of A Zero Coupon Bond?

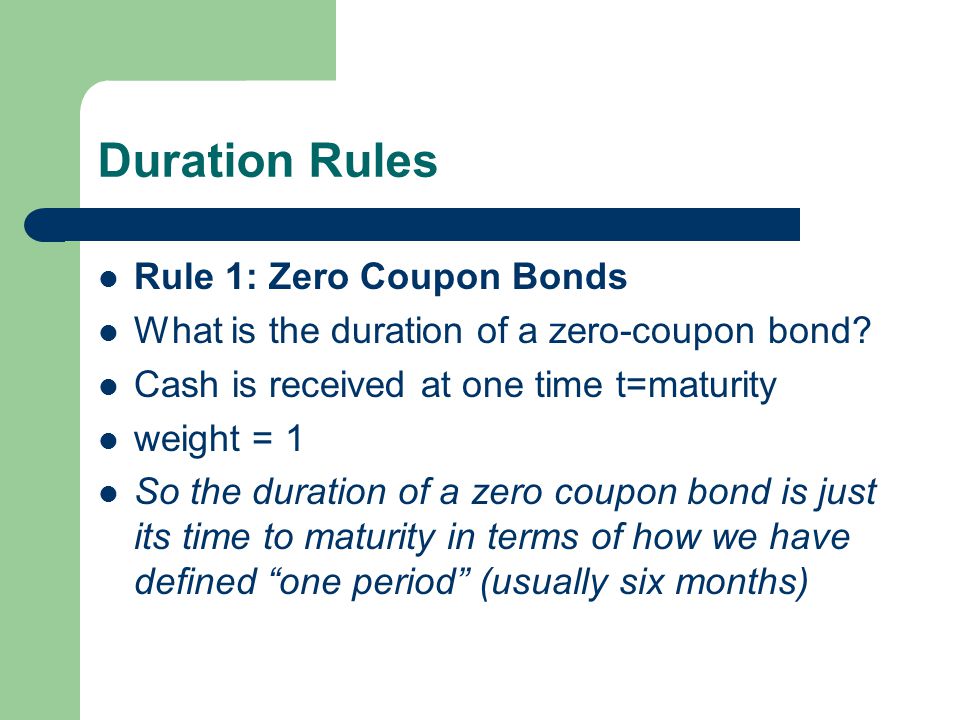

Interest-Rate Risk II. Duration Rules Rule 1: Zero Coupon ...

Solved You are managing a portfolio of $1.0 million. Your ...

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Post a Comment for "44 duration zero coupon bond"